Must read – Composite Supply under GST Regime But not all supplies will be such simple and clearly identifiable supplies. Some of the supplies will be a combination of goods or combination of services or combination of goods and services both. Each individual component in a given supply may attract different rate of tax. The rate of tax to be levied on such supplies may pose a problem in respect of classification of such supplies. It is for this reason, that the GST Law identifies composite supplies and mixed supplies and provides certainty in respect of tax treatment under GST for such supplies.

Mixed Supply under GST

Under GST, a mixed supply means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply: Illustration: A supply of a package consisting of canned foods, sweets, chocolates, cakes, dry fruits, aerated drinks and fruit juices when supplied for a single, price is a mixed supply. Each of these items can be supplied separately and is not dependent on any other. It shall not be a mixed supply if these items are supplied separately In order to identify if the particular supply is a mixed supply, the first requisite is to rule out that the supply is a composite supply. A supply can be a mixed supply only if it is not a composite supply. As a corollary it can be said that if the transaction consists of supplies not naturally bundled in the ordinary course of business then it would be a mixed supply. Once the amenability of the transaction as a composite supply is ruledout, it would be a mixed supply, classified in terms of supply of goods or services attracting highest rate of tax The following illustration given in the Education Guide of CBEC referred above can be a pointer towards a mixed supply of services: A house is given on rent one floor of which is to be used as residence and the other for housing a printing press. Such renting for two different purposes is not naturally bundled in the ordinary course of business. Therefore, if a single rent deed is executed it will be treated as a service comprising entirely of such service which attracts highest liability of service tax. In this case, renting for use as residence is a negative list service while renting for non-residence use is chargeable to tax. Since the latter category attracts highest liability of service tax amongst the two services bundled together, the entire bundle would be treated as renting of commercial property.

Tax Rate applicable to Mixed Supplies

As per section 8(b) of CGST Act, the tax liability on a mixed supply comprising two or more supplies shall be treated as a supply of that particular supply which attracts the highest rate of tax

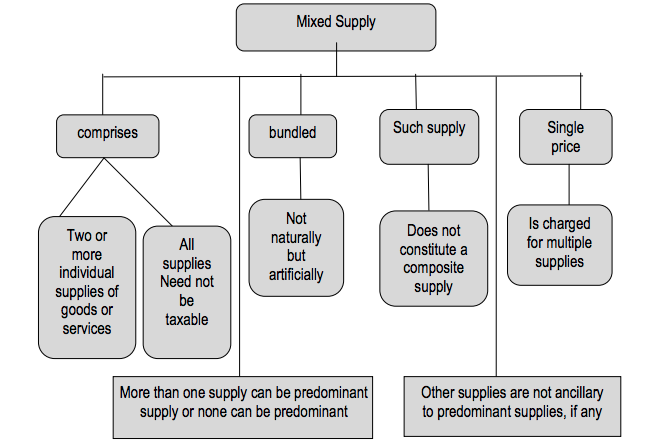

Features of Mixed Supply

Features of Mixed Supply are as under:

(a) Mixed Supply consists of two or more individual supplies.(b) Supplies are not naturally bundled.(c) One of the supplies may not be principal supply and other supplies need not be ancillary supplies.(d) All the supplies need not be taxable supplies. Even non- taxable supplies along with taxable supplies can constitute mixed supply.(e) Supply does not fall within the definition of composite supply.(f) A single price is charged for multiple supplies.

Example: A supply of a package consisting of canned foods, sweets, chocolates, cakes, dry fruits, aerated drinks and fruit juices when supplied for a single price is a mixed supply. Each of these items can be supplied separately and is not dependent on any other. It shall not be a mixed supply if these items are supplied separately In order to identify if a particular supply is a mixed supply, the first requisite is to rule out that the supply is a composite supply. A supply can be a mixed supply only if it is not a composite supply. If the transaction consists of supplies not naturally bundled in the ordinary course of business, then it would be a mixed supply. Once the amenability of the transaction as a composite supply is ruled out, it would be a mixed supply, classified in terms of supply of goods or services attracting highest rate of tax. A house is given on rent, one floor of which is to be used as residence and the other for housing a printing press. Such renting for two different purposes is not naturally bundled in the ordinary course of business. Therefore, if a single rent deed is executed it will be treated as a service comprising entirely of such service which attracts highest liability of service tax. In this case, renting for use as residence is an exempt service while renting for non-residential use is chargeable to tax. Since the latter category attracts highest liability of service tax amongst the two services bundled together, the entire bundle would be treated as renting of commercial property. Other Examples of Mixed Supply:

Tooth brush with tooth pasteSoap with detergentBiscuits with chips etc.

Determination of tax liability of composite and mixed supplies

The tax liability on a composite or a mixed supply shall be determined in the following manner:

(a) A composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply(b) A mixed supply comprising two or more supplies shall be treated as a supply of that particular supply which attracts the highest rate of tax

Time of supply in case of mixed supplies

The mixed supply, involving supply of a service liable to tax at higher rates than any other constituent supplies, would qualify as supply of services and accordingly the provisions relating to time of supply of services would be applicable. Alternatively, the mixed supply, involving supply of goods liable to tax at higher rates than any other constituent supplies, would qualify as supply of goods and accordingly the provisions relating to time of supply of services would be applicable. Recommended Articles

GST ScopeGST ReturnGST FormsGST RateGST RegistrationWhat is GST?GST Invoice FormatGST Composition SchemeHSN CodeGST LoginGST RulesGST StatusTrack GST ARNTime of Supply